It needs a number of wonky adjustments, not a dramatic overhaul.

It needs a number of wonky adjustments, not a dramatic overhaul.

Other than a fairly vague “we know it’s not perfect”, elected Democrats have been reluctant to criticize ObamaCare while it was facing the prospect of a full repeal. Even fairly mild criticism, they feared, might lead to “Even Democrats Hate ObamaCare” headlines and feed the repeal movement. Worse, if Democrats settled on a fix-ObamaCare plan, McConnell and Ryan might take one or two minor ideas from it and claim that their new repeal plan was bipartisan, even as it gutted the larger purpose of ObamaCare.

But even though ObamaCare repeal keeps rising from the dead, maybe the its most recent defeat leaves an opening for an honest effort to improve the system. That will be tricky, because it means putting aside an enormous amount of widely believed lies and focusing on what the real problems are.

What ObamaCare was supposed to do. One reason all the Republican repeal-and-replace bills have been so unpopular is that no one could say exactly what they were supposed to accomplish, other than fulfill the promise to repeal ObamaCare. Repeal has become an end in itself, independent of anything it might do to help or hurt the American people.

By contrast, all Democratic healthcare plans are based on a simple principle: Sick or injured people should get the care they need, and they shouldn’t have to go bankrupt paying for it. Large majorities of Americans believe in that vision, and Democrats have been trying for decades to make it real. ObamaCare has always been an imperfect implementation, but it was a significant step in the right direction.

Why not single-payer? The most direct (and, in my opinion, the most efficient) way to implement that principle is some kind of single-payer, Medicare-for-all system like just about every other advanced country already has. It’s been tested in nations all over the world, and it works. Germany or Australia, for example, spend far less per capita than we do on healthcare, and their people live longer. [Update: See the comments for a correction. I have used “single-payer” as a synonym for “universal health insurance”, which is not accurate. In particular, Germany achieves universal coverage differently.]

I suspect that in their hearts, all the Democrats running for president in 2008 would have preferred a single-payer system, but most of them believed Congress would never pass it. So Obama and his main competitors (Hillary Clinton and John Edwards) all proposed very similar systems, roughly based on the program that Republican Governor Mitt Romney had already started in Massachusetts. Dennis Kucinich had the single-payer supporters all to himself in the New Hampshire primary, where he got 1.35% of the vote.

Single-payer advocates find this kind of timidity mysterious — or they attribute it to bribery by the big insurance companies — because if you poll single-payer by itself, it does pretty well. So why not go for it?

What makes even honest politicians nervous is that lots of things poll well until a campaign begins, when the negative ads and outright lies start to fly. HillaryCare polled well at first too, until Republicans and insurance companies started going after it. In no time it all, it morphed from an unstoppably popular proposal to the reason the Democrats lost the House in 1994.

Whenever a proposal fails, you can point to plenty of mistakes its backers made. (Supporters of successful proposals also make a lot of mistake, which are quickly forgotten.) But it also seems to be true that the American people harbor a deep well of distrust for politicians and their promises. If a negative ad tells people you’re going to take something away from them, they believe it. If you respond that you’re going to give them something better, they don’t.

Nobody wants to believe that this applies to them as well as their opponents, but it does. Republicans, I’m sure, have been shocked these last six months to discover that many of the same people who distrusted ObamaCare now distrust their replacement plans even more. (ObamaCare repeal as an abstract idea has long polled in the 40s. All the specific repeal bills discussed recently have polled in the teens.) As soon as Republicans gained enough power to implement actual changes, they became the new owners of the well of distrust.

Single-payer supporters on the Democratic left are making a similar mistake today, I believe, when they imagine that the wave of public distrust they’ve helped raise against establishment Democrats won’t wash back on them if they ever take power.

Three options. When you come down to it, there are really only three ways government can handle the problem of the uninsured.

- Ignore it. When the uninsured get sick, either private charity will take care of them or they’ll die.

- Have one system that covers everybody.

- Have a crazy-quilt of different programs that all have their own rules and justifications, and hope that not that many people slip through the gaps.

ObamaCare is a type-3 plan. TrumpCare failed because it could never decide whether it was a type-1 plan or just another type-3 plan with more gaps.

The ObamaCare Rube Goldberg machine. Public distrust of change is one major reason ObamaCare was designed to minimize the number of people facing significant disruption. If you got your healthcare through Medicare, Medicaid, the VA, or your employer’s group plan (like my wife and I did and do), you probably didn’t notice much difference. Obama’s “If you like your health plan you can keep it” may have been Politifact’s Lie of the Year, but it was actually more of an exaggeration than a lie. After the ACA passed, the vast majority of people with good health insurance just kept doing whatever they’d been doing.

Maintaining all those legacy programs guaranteed that covering the uninsured would be complicated. So ObamaCare covered uninsured people like this:

- The poor continue to get Medicaid.

- Those just above the poverty line — who presumably can manage day-to-day expenses like food and rent, but have nothing left over to insure against emergencies — get covered by extending Medicaid (though the Supreme Court allowed states to opt out of this).

- Low-to-middle working-class people whose jobs don’t include health insurance can get a subsidy to buy individual insurance on an ObamaCare exchange. (The subsidies phase out as incomes increase.)

- Better-off people whose jobs don’t include health insurance can buy policies on the exchanges at full price.

Gaming the system. In addition to the complexity of how you got covered, there were changes in the rules of coverage. Mostly, this is about keeping players from gaming the system.

When insurance companies compete on price and service, the public benefits. But prior to ObamaCare, a lot of insurance competition was about something else: making sure that their own insurance pool was healthier than the other companies’. So insurers got really good at figuring out who was a bad risk and cancelling their polices. That helped the company’s bottom line, but was bad for public health. (And if your wife is a cancer survivor, it’s terrifying.)

So the biggest (and most popular) rule change was that insurance companies have to offer coverage to everybody, no matter how unhealthy they are or might get. Nobody is uninsurable any more.

But that created a new opportunity to game this system: Healthy individuals might go without insurance, figuring that they could pick it up later if they ever needed it. Taking healthy people out of the insurance pool ruins the whole idea of insurance — imagine if you could put off buying fire insurance until after your house burned — so that had to be prevented somehow. That’s where the individual mandate comes in: Even if you’re healthy, you either carry insurance or pay a tax.

So

- no discrimination against pre-existing conditions,

- a mandate for individuals to carry insurance, and

- subsidies so that even individuals just above the poverty line can afford the insurance they’re obligated to carry

is sometimes called the “three-legged stool” of ObamaCare. The system is unstable unless you have all three.

Where there are problems. The problems with ObamaCare have been wildly exaggerated by Republican talk of a “meltdown” or “collapse” or “death spiral“. But ObamaCare has run into three main problems:

- The Supreme Court allowed states to opt out of Medicaid expansion, and a number of the red states have, at great cost to their citizens and hospitals. Policies on the ObamaCare exchanges are not designed for households near the poverty line; the deductibles on the cheapest (bronze) plans are far too high for them, and they may not qualify for the subsidies. The Medicaid-denied people who do sign up on the exchanges tend to be the very sick, whose expenses raise premiums for everyone.

- Not enough healthy people are signing up to keep premiums low. The original projections didn’t anticipate that HHS would use its PR budget to undermine ObamaCare [1], that private sources would launch a well-funded advertising campaign against signing up, or that refusing to sign up would become part of a political identity.

- Not enough insurance companies are participating (particularly in rural areas [2]) to keep the exchanges competitive.

The last two should not be all that surprising. If you look at the description of ObamaCare above, it depends on inducing people to cooperate, not forcing them. (That’s why it’s ironic that it’s been attacked as an assault on “freedom”.) For the program to work smoothly, the inducements — subsidies to individuals, reinsurance for insurance companies, the income level where Medicaid expansion ends and private-sector policies begin, the tax on the uninsured — have to be calibrated right.

Healthcare experts made their best estimates when the law was written, but everyone expected to make adjustments as the real-world results started coming in. This is not unusual with big new social programs. Social Security, Medicare, and Medicaid all required some fine-tuning as they got off the ground, and still get re-jiggered periodically.

But no one foresaw that Republicans would immediately gain control of the House, and then take the attitude that the only acceptable adjustment was complete repeal. It’s hard to grasp now how big a change this is from all previous American history. Typically, opposition parties in America have not tried to sabotage programs they disapprove of. Until the current era, small changes that improve the working of an existing program have been uncontroversial, even among congresspeople who voted against the program originally.

The sabotage problem has gotten worse since Trump became president. He gleefully talks about letting ObamaCare implode, and creates uncertainty in the insurance markets by threatening to delay or withhold payments. Insurance is all about managing risk, so adding any new uncertainties to the system is monkey-wrenching.

How to fix them (if you want to). It should go without saying that the first step in fixing something is to stop trying to break it. But beyond that, there are some obvious things to do.

Ten House Democrats — including my NH-2 rep, Annie Kuster — have put out a plan to stabilize the individual insurance markets. The main planks are:

- a permanent reinsurance program to protect insurers against unexpectedly high claims. This would encourage insurers to compete in more markets. ObamaCare had such a program initially, but it has expired.

- reduce deductibles and co-pays for people with low incomes. There’s already a program in the ACA that does this: The government is supposed to make “cost sharing reduction” payments to insurance companies that keep these costs low. But there’s a dispute working its way through the courts about whether Congress has to appropriate this money year-by-year (which it hasn’t done) and Trump is threatening to withhold the payments.

- market better. HHS needs to start spending its advertising budget to promote ObamaCare rather than denigrate it. One simple suggestion: Make the ObamaCare open enrollment period line up with the April 15 tax deadline, so that people who have just seen how the tax subsidies and the individual mandate affect them could immediately take action for next year.

- enforce the individual mandate, which the IRS is currently not doing.

- let people over 55 buy into Medicare. This will shift some of the most expensive people out of the ObamaCare risk pools, lowering premiums for everyone else.

- give bigger subsidies to older people in rural areas.

Other ideas are out there as well. Saturday’s NYT listed at least two (in addition to some of the ideas already mentioned).

- reduce drug prices. If there’s real competition, then anything that makes healthcare less expensive makes health insurance less expensive. At the very least, lower drug prices would help people who have high deductibles and co-pays. And everyone agrees that the current system — which lets drug companies with patents dictate a price which the government and insurance companies are obligated to pay — is rigged in drug companies’ favor. Part of the Democrats’ “Better Deal” proposal is a federal agency that guards against price gouging.

- extend ObamaCare-exchange subsidies to people in the Medicaid gap. It’s crazy that many states still haven’t accepted Medicaid expansion, but that seems to be the way it is.

538 passes on something clever Nevada is doing: Insurers who offer plans on the ObamaCare exchange in Nevada are more likely to be chosen to manage the state’s Medicaid plan. A similar idea (which I didn’t invent, but can’t remember where I saw it) is to force insurers who want to compete in lucrative urban markets to also cover rural areas.

Mending is boring, but insurance ought to be boring. None of this is the kind of sweeping change that inspires people. It’s more like when a football team works on blocking and tackling better, rather than coming up with new trick plays.

But it also shouldn’t scare people. The original structure of the plan is still sound. It just needs some adjustments.

The question is whether congressional Republicans want to make those adjustments, or the Trump administration wants to implement them. They can, if they want, make ObamaCare collapse.

If they do that, though, they may convince the public that type-3 crazy-quilt plans don’t work. And if the public has to choose between a type-1 let-them-die program and a type-2 Medicare-for-all plan, I don’t think Republicans will like how that decision comes out.

[1] The Daily Beast reports:

To date, [HHS] has released 23 videos. A source familiar with the video production says that there have been nearly 30 interviews conducted in total, from which more than 130 videos have been produced.

Each testimonial has the same look, feel, and setting, with the subjects sitting before a gray backdrop and speaking directly to camera about how Obamacare has harmed their lives. They were all shot at the Department’s internal studio, according to numerous sources who worked for or continue to work at HHS.

The videos openly suggest Congress repeal ObamaCare. The one featuring Robert Dean ends like this:

I really hope that the Trump administration and the U. S. Congress, Republicans in the Senate and House, can get their act together and deliver relief to the American people.

Given this openly political — and even partisan — message, I suspect that spending public money to produce and distribute these videos is illegal. If HHS Secretary Tom Price knew about this and condoned it, he should resign.

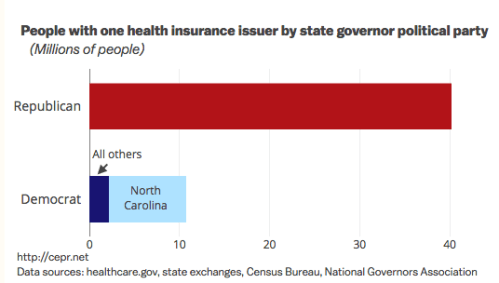

[2] As the liberal Center for Economic Policy and Research think tank notes, lack of competitive exchanges is particularly a problem in Republican states that have done their best not to cooperate with ObamaCare. It provides the following chart:

In part this is a coincidence caused by the fact that largely rural states tend to have Republican governors. But so is the frequently cited statistic that 1/3 of counties have only one insurer: Those counties tend to be sparsely populated, so the number of people they represent is far less than 1/3 of the country.

The are lots of reasons why rural areas are especially hard hit. Most obviously: Having fewer people makes them a less robust insurance pool, increasing risk to the insurer. Also, healthy young people tend to seek opportunity in the bigger cities, leaving older, sicker people behind.

Comments

Let us remember that at the core of Republican opposition to the ACA is pure and simple racism.

I wonder if that has less juice now that Obama is gone.

It does not.

As long as the name “Obama” is there, it’s about race. Or ather, it is for the foolish republican voters who never bothered to understand why our healthcare system sucks and the origins of the ACA.

The republican senators and congresspeople may have unconscious racist tendencies but I’m betting that it’s more about the money. Rich people are God’s chosen people. Businesses are temples. The poor are inherently unworthy because they are not rich. And politicians need money to run re-election campaigns.

They aren’t stupid people (well, except for a few such as Gohmert). Their aides aren’t stupid HS drop outs who never bothered to open a book after the 8th grade. They know exactly what they are doing when they have their skinny repeals or their horrible alt-republican healthcare replacement bill. Right now, they are trying to figure out how to get more tax rights offs for the wealthy because they subscribe to the Ayn Rand world view of business rather than the reality of how businesses will run.

Those HHS videos are ridiculous and certainly have to be illegal! Spending public funds to take a partisan stand?? Who can take that issue on? Also love how they disabled comments so no one can post responses about how they have been helped by the ACA.

“…Tom Price… should resign.”

Hahahahahahahahahahahahahahahahahahahaha…!!!

It’s been a long time since a Republican has done what should be done. Don’t hold your breath!

I like a lot of what you’ve said here but wanted to point out that Germany does NOT have a single payer system. It’s a universal “multi-payer” system that uses both public and private funds. I used to be a staunch advocate of single payer but lately have changed my mind, mainly because I think this kind of universal multi-payer system will be much easier to reach from what we have now in the US. And there’s no reason that it can’t deliver quality affordable healthcare for all. Plenty of other countries around the world have demonstrated that this kind of hybrid works.

er, public and private insurance. http://www.germanyhis.com

This study by T.R. Reid, entitled “The Healing of America” (2009 – still relevant, unfortunately), is a good compendium of health care plans in the world’s major industrialized nations. For those who (like me) feel that the US doesn’t have to reinvent the wheel on healthcare, give this book a read.

https://en.wikipedia.org/wiki/The_Healing_of_America

Thanks for the correction.

Lisa, Germany does have a multi-payer system BUT the insurers are all non-profit and highly regulated. I am just not sure it would be any easier to make all insurers non-profit and pass all the regulations to create a Bismark-type system (which the insurance companies would fight tooth and nail) than it would be just to set up a single payer system.

This process is FINALLY moving in the right direction!

https://www.alexander.senate.gov/public/index.cfm/2017/8/chairman-alexander-and-ranking-member-murray-announce-health-care-committee-hearings

Trackbacks

[…] week’s featured post is “How to Fix ObamaCare“. The “Misunderstood Things” series is taking a week […]

[…] Some Republican senators are looking for a bipartisan fix for the ObamaCare exchanges (along the lines I discussed last week). […]