President Obama’s legacy accomplishment has problems that can be patched up. But will they be?

In the insurance business, the big thing you worry about is a vicious cycle called a “death spiral”. It goes like this:

- An insurance company realizes it isn’t making enough money because it’s paying more claims than expected. In other words, the risk pool is riskier than it predicted.

- It tries to increase profits by raising premiums.

- Supply-and-demand works in the usual way, so the increased price causes fewer people to want the product. But because of the unique properties of insurance, the people who drop coverage are mostly the ones who think they are less likely to make claims; the insurance was worth it to them at the old price, but not at the new. Meanwhile, the high-risk customers, the ones who will want insurance at virtually any price, all stay.

- As the low-risk customers defect, the risk pool gets even riskier. So the insurance company is back at Step 1, paying too many claims to make the profit it wants.

To a certain extent this cycle happens whenever an insurance company underestimates risk or overestimates the number of people who will want its coverage. But usually the effect damps out. In other words, each time around the cycle, fewer and fewer people drop coverage at Step 3, so after some small number of price hikes, a new equilibrium is reached: The higher premium covers a smaller, riskier insurance pool while still leaving the company a profit.

But in a death spiral, the cycle never damps out and there is no new equilibrium. Or, more precisely, the equilibrium point everything trends towards is zero: No one is covered, so the zero premiums balance the zero claims.

Now let’s talk about ObamaCare: Millions of people have signed up for insurance through the ObamaCare exchanges, but not as many as expected. In particular, not as many young, relatively healthy people have signed up. So the total covered population is sicklier than the insurance companies had planned on, and they’re not making money the way they thought they would.

So Step 2 is starting to happen: Last Monday, a report from the Department of Health and Human Services (HHS) said that baseline premiums on the ObamaCare exchanges would be going up 22% on average. In addition, some insurance companies have decided to pull out of the ObamaCare marketplace in a various states, reducing competition and making it easier for the remaining insurers to raise premiums.

That raises the question: Is this a blip that will quickly settle out into a new equilibrium, or is it the start of a death spiral?

It’s hard to get good information on this, because everyone knows which answer they want: Conservatives want a death spiral, and liberals want a blip.

Underenrollment. Let’s start with numbers. Back in 2010, the Congressional Budget Office projected much higher enrollment than we’ve seen.

CBO and [the Joint Committee on Taxation] project that, under current law, 6 million people in 2014 will receive insurance coverage through the new exchanges. Over time, more people are expected to respond to the new coverage options, so enrollment is projected to increase sharply in 2015 and 2016. Starting in 2017, between 24 million and 25 million people are expected to obtain coverage each year through exchanges, and roughly 80 percent of those enrollees are expected to receive subsidies for purchasing that insurance.

That didn’t happen. 2016 enrollment through the exchanges was about half the projection, around 10.4 million, and (prior to the premium increases) the most optimistic estimates projected around 13 million for 2017.

You can argue about why. Maybe the carrots (subsidies) and sticks (the individual mandate’s tax on the uninsured) weren’t as compelling as they should have been. Or maybe the scorched-earth nature of Republican resistance made a partisan issue out of decisions that (in an alternate universe) might have seemed public-spirited. Larry Leavitt pictures that alternate universe:

Imagine a world where the ACA passed with significant bipartisan support and there was a national effort involving politicians of all stripes and figures, and athletes, all encouraging people to get insured. That is not the world we live in. It’s more like what happened in Massachusetts [with RomneyCare].

Instead, we saw something altogether unprecedented in American history: a well-funded ad campaign trying to convince people to avoid a government program that had already been enacted into law. Who can forget the Koch Brothers’ creepy Uncle Sam who was going to “play doctor” with you?

For comparison, try to imagine it’s 1942 and some anti-war billionaires blanket the country with creepy Uncle Sam posters to convince people not to buy war bonds, or it’s 1966 and ads interrupt The Beverly Hillbillies to scare seniors out of signing up for Medicare. Nothing remotely like that happened or could have happened under the political culture of those eras. But it did for us.

Premiums. One important thing to realize about ObamaCare premiums is that up until now they’ve been running under the original projections.

There are a variety reasons for that: In part, it’s that healthcare inflation in general has been lower since the Affordable Care Act started coming into effect.

But a piece of it is also that insurance companies lowballed their initial offers, hoping that once people had health insurance they’d be reluctant to give it up or switch companies. The LAT’s Michael Hiltzik reports:

But a piece of it is also that insurance companies lowballed their initial offers, hoping that once people had health insurance they’d be reluctant to give it up or switch companies. The LAT’s Michael Hiltzik reports:

Some big insurers have found that their initial estimates of customer costs were unduly optimistic. They set premiums lower than they should have, sometimes to buy market share, and incurred losses as a result. Rate-increase requests in the double-digit range for 2017 are the harvest

So what looks like a malfunction in the program might just be premiums getting back to the level they should have been at to begin with.

Subsidies. One reason to think that the premium increases won’t start a death spiral is that most of the people who use the federal exchanges get some amount of subsidy. As their premiums go up, their subsidies do as well. So the sticker shock is diminished.

The people to watch are the ones whose incomes are too high to qualify for subsidies. According to Leavitt, that’s about 15% of the people who use the federal exchanges, but also almost seven million other people whose premiums are based on the rates on the federal exchanges (and whose business the insurance companies are figuring in when they set their premiums). If those people start cancelling their policies, then we could be back in the death-spiral scenario. But if they decide that they like having health insurance and are willing to pay the higher premium to keep it, then everything should be fine.

Fixes. Even if the vicious cycle starts, there are fairly simple ways to stop it — if that’s what everyone wants to do. Basically, the problem, if there turns out to be one, is that the incentives aren’t right yet: The subsidies need to be higher or extend to people with somewhat higher incomes. Or the individual-mandate penalty on the uninsured (the one you would pay when you file your 1040 income tax form) needs to be higher.

Other things could be done to lower insurer costs: The sign-up periods might be tighter and more strictly enforced, to prevent people from abusing the system by waiting until they get sick to get covered. Price controls could prevent profiteering by big pharmaceutical or medical-device companies. The bundle of services that need to be included in an ObamaCare policy could shrink.

Or you could change the market in other ways: In parts of the country (like Arizona) where premiums are rising faster because fewer companies compete, adding a public option (i.e., something like letting you buy into Medicare even if you’re not 65 yet) would increase competition.

Or if you want to go whole hog, the entire health-insurance system could be replaced by some kind of single-payer system, as Bernie Sanders campaigned on, and as gets better outcomes for less expense in just about any other advanced country.

The problem is getting any of that through Congress. So far, Republicans have refused to cooperate in making any mid-course adjustments to ObamaCare, in hopes that it will crash. This also is brand new in American politics. Previous programs like Social Security, Medicare, and even the prescription-drug benefit that President Bush added to Medicare in 2003 all have required tweaks as they got up and running. Once a program had been passed into law, Congress typically has accepted it and tried to make it work. But scorched-earth opposition to ObamaCare continues six years after the law passed: The only change Republicans are willing to consider is repeal.

The problem is getting any of that through Congress. So far, Republicans have refused to cooperate in making any mid-course adjustments to ObamaCare, in hopes that it will crash. This also is brand new in American politics. Previous programs like Social Security, Medicare, and even the prescription-drug benefit that President Bush added to Medicare in 2003 all have required tweaks as they got up and running. Once a program had been passed into law, Congress typically has accepted it and tried to make it work. But scorched-earth opposition to ObamaCare continues six years after the law passed: The only change Republicans are willing to consider is repeal.

We can’t go back. In the same way that President Obama’s economic critics often conveniently forget how the economy was collapsing when he took office, critics of ObamaCare forget how the old healthcare system was collapsing under the middle class. The poor could get Medicaid, but health insurance was increasingly out of reach for people who weren’t covered through their employers, and employers faced rising pressure to wriggle out of rapidly increasing premiums.

As a result, the number of Americans with no health insurance at all was approaching 50 million. Millions more Americans had “junk insurance” — low-maximum-benefit policies that would quickly be exhausted by any major illness, or short-term policies the insurer could refuse to renew if you got seriously ill. (Many of the much-publicized horror stories about premiums that skyrocketed when ObamaCare took effect were from people who previously had junk insurance. They didn’t pay much, but they would still face bankruptcy if they got seriously ill.) No one knows how many people were trapped in jobs they couldn’t leave because their pre-existing conditions would prevent them from qualifying for health insurance with a new employer.

In 2009, Time correspondent Karen Tumulty drew the lesson from her brother’s inability to pay for his medical care, even though he had insurance when he got sick.

What makes these cases terrifying, in addition to heartbreaking, is that they reveal the hard truth about this country’s health-care system: just about anyone could be one bad diagnosis away from financial ruin.

As the so-called “gig economy” grows, the lifetime-employment ideal of the 20th century is realized for fewer and fewer people, exposing more and more people to gaps in their healthcare coverage that they may not be able to fill due to pre-existing conditions. So going back to the system that was already starting to fail in 2010 would be trading a fixable death spiral for an inescapable one.

Replace? “Repeal and replace” has been the Republican slogan since 2010, but the “replace” part never materializes. Some vague ideas are thrown around: insurance competition across state lines, health savings accounts, and so on. But the discussion always stops short of an actual bill that the CBO could analyze and members of Congress could be asked to support or oppose.

Most likely that’s because the numbers don’t work, either in an accounting sense or a political one. Paul Ryan and Mitch McConnell know they can’t assemble their fractious troops behind any specific proposal. And if they did, the resulting plan would vastly increase the number of uninsured people, while leaving those with insurance vulnerable to losing it if they get sick or change jobs.

The basic vision of ObamaCare — private health insurance made universal through a system of government mandates and subsidies — was created by conservatives who wanted an alternative to a single-payer system. More than 20 years later, those are still the only two viable ideas out there. If you really want to replace ObamaCare, single-payer is your only choice. If that’s not what you want, then you should help fix ObamaCare.

Comments

I’ll listen to the REpubs when they actually put out a replacement plan.

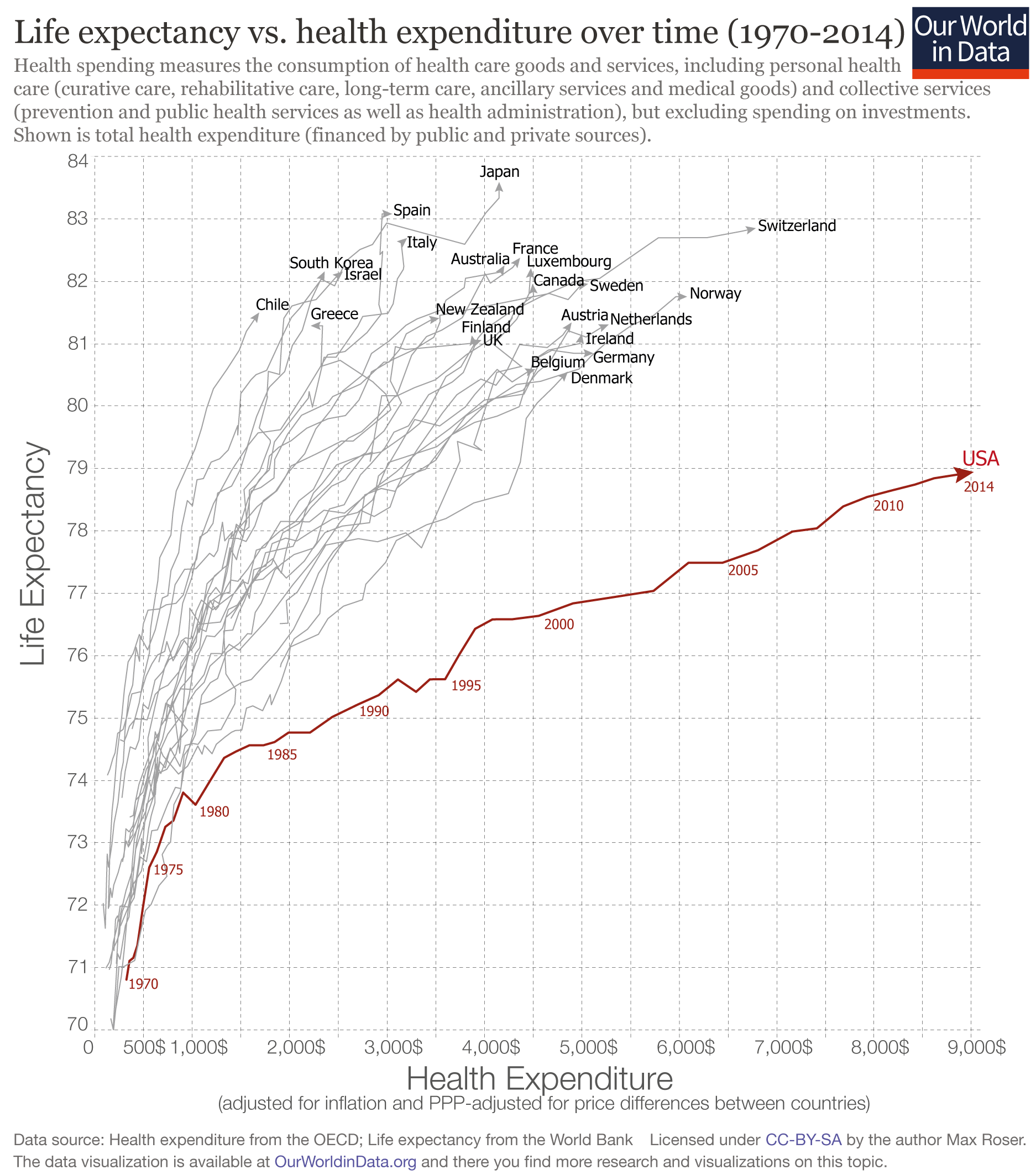

A-way back in 1976, I did a legislative analysis of a proposed national health insurance bill (Kennedy-Corman). Health expenditures were accelerating and approaching 7% of GNP which would make health care the largest domestic industry. Our analysis suggested that, without changes, the health sector would, at an ever increasing pace, continue to consume a greater percentage of GNP. The graph from OurWorldinData.org reflects this result quite dramatically. Another graph from OurWorldinData.org, which you don’t display, shows that the expenditures are concentrated very tightly in a small number of people. They say: “The following graph shows this inequality. The top 5% of spenders accounts for almost half of all health care spending in the US.” I’m not quite sure how to interpret this though I assume it reflects, in part, our tendency to respond to crises and shortchange preventive care — kind of like scheduled maintenance (oil changes) versus breakdowns (replacing the engine). The question is one of how do we achieve universal coverage and, at the same time, reverse ever-accelerating expenditures. I question how a market-based approach, at least in this country, will resolve this.

There’s a decent article at DKos on this as well.

http://www.dailykos.com/stories/2016/10/30/1587345/-What-s-behind-the-healthcare-rate-hikes-and-7-other-things-Donald-won-t-tell-you-about-the-ACA

s

Any successful business model requires objective evaluation of inputs and outputs, formulating and implementing policy based on that information, subsequently carefully measuring and analyzing feedback, objectively analyzing feedback results, and adjusting/abandoning/reformulating policy so as to reconcile performance with reality so as to increase efficiency and achieve optimum performance at best obtainable cost.

GOP governmental performance strategy since Reagan is entirely captured by ideological zealots too slavishly devoted to doctrine to be able to separate from it far enough to achieve even a minimally useful perspective on their ideological doctrinal outcomes — they self-deny objective monitoring of feedback and wind up trapped in an endless repeating loop of failure.

Democrats aided and abetted, beginning in the 70s when they were coming to the close of 3.5 decades of House (budgetary) control, by deliberately stepping off firm fiduciary footing into the swamp of neoliberal economic policy.

Only recently (thanks Bernie candidacy/followers) has the Party platform included planks which deviate from the neoliberal agenda, and it remains to be seen if an elected HRC will hue to this platform, or post-election stubbornly persist in the policies she advocated prior to the pressure from the progressive wing early this summer.

I see single-payer as the only existing pragmatic health care option, and it is not a possible option within the neoliberal realm.

Hillary will have to negotiate with Congress, which will be at least half-controlled by Republicans. So she won’t get much of Bernie’s agenda enacted into law, and President Sanders wouldn’t have either.

And how do we get there from here? SPIN is important — what is the SItuation…what is the Problem….what are the Implications….what are the Needs. I’d like to see Medicare eligibility expanded. I’d like to think that this might create momentum as others will want to belong. Ultimately, one would think that employers wouldn’t mind letting go of their paying and administering health benefits.

” No one knows how many people were trapped in jobs they couldn’t leave because their pre-existing conditions would prevent them from qualifying for health insurance with a new employer.”

That particular problem could be solved by COBRA. Under the current COBRA law, you can keep your existing health insurance for 18 months after you leave your job if you continue to pay the premiums yourself. If you remove the end date, then anyone can keep their coverage for as long as they continue to pay the premiums. That one change also takes care of a bunch of problems with the “gig-economy”

Yes, COBRA offers an 18 month extension of one’s exit job insurance; however, not at the same cost you were paying while working for said company because you will be paying the full premium, not just the employer co-pay. Once the 18 months is up, you are on your own…The beauty of the ACA is that you will not be denied coverage due to a pre-existing health condition, nor can you be charged more for having one.

The stated goals of health care reform in 2009 (Obamacare) in the USA were

1.lower costs

2.cover all Americans

3.drive quality

4.and be paid for (without impacting the federal budget)

However there is no provisions in the ACA to control costs. That is the flaw in Obamacare. In a country where “for profit” takes priority over almost everything else this should not come as a surprise. I continue to hear people say they oppose socialize medicine. No one has offered an alternative to for profit health care. We have no one to blame but ourselves for the kind of health care in America.

There are many cost reductions as a result of the ACA but most people don’t recognize them. (1) insurance rates cannot be higher due to pre-existing condition nor can people be denied coverage based upon said conditiions…before, you had to shop for an individual policy where your medical underwriting dictated your premium; (2) Medicare participants have free annual health care screenings with many basic tests covered; (3) Medicare participants “doughnut” hole is shrinking, thereby reducing participant out of pocket costs for prescriptions; (4) Hospitals are having to reduce charges to meet ACA guidelines; (5) insurance companies MUST spend 85% of their revenue on direct patient related care, IOW, profits are limited to a maximum of 15%….and there are many more…

ACA made good strides toward universal coverage and tries to limit some aspects of insurance cost, but it does not address healthcare costs, and without controlling them, insurance costs cannot be controlled (especially when the providers are private profit-seeking entities). Controlling healthcare costs is key, and that means drug costs, preventative care, runaway medical procedures, and infrastructure (eg, hospitals) costs that serve profit motives rather than better healthcare. It is hard for me to see how this happens without significant government leadership and regulation, both of which seem hard to come by these days. “Which side are you on….”

When the Republican Congress passed Pres. GW Bush’ Medicare Part D (RX plan), the pharmaceutical lobby explicitly lobbied and got, a provision in the bill that prohibits the federal government from price negotiations for drugs for this plan (as VA and Medicaid do). This means the government/aka “taxpayer”, pay full prices for all meds which costs are spiraling out of control.

The only way this can be changed is by Congressional action.

Vote Democrat this election.

In Minnesota for the MNSure exchange, premiums have increased 50% to 67% for 2017. Two larger insurers, United Healthcare and Blue Cross Blue Shield have left the exchange, leaving many, many people in jeopardy. Platinum policies disappeared in 2016 completely. If you needed that kind of coverage, you had to buy it off the exchange and the one time I checked, the premiums were about $1000 per month for individual coverage. I was in Minnesota’s high risk pool for years and was looking forward to the ACA and lower premiums. I went from almost $800 a month in the high risk pool to about $400 a month with a subsidy paying the rest the first year. It went downhill after that. Now I’m on the state’s Medicaid insurance because paying for the premiums from 2014 on wiped out my savings and I don’t make enough to qualify for anything else. I need platinum coverage because of pre-existing conditions. I wish I could just sign up for Medicare now! Cinda

As a Bernie supporter (and now Hillary supporter :-), I approach healthcare reform from the left, and i think Obamacare is an utter failure in all its stated goals. I agree with Dean when he said long ago that we should junk it and start over, even if we don’t get the chance to do that for another 20 years.

Firstly, 70% of the people who got insurance under Obamacare came from expanding medicaid eligibility. That had nothing to do with the health insurance reforms that form the heart of Obamacare, and to claim that Obamacare reduced the rolls of the uninsured without acknowledging that only 30% comes from Obamacare per se, is disingenuous.

Secondly, in exchange for removing lifetime caps and pre-existing conditions, Obamacare plans have deductibles of $6500/person and $12000/family. This is only a good deal *if you can afford the deductible*. If an unexpected expense of $6500 will throw you into bankruptcy anyway, then it doesn’t really matter whether the insurance plan has lifetime caps or not: the result to your financial health is the exact same. I wish I could find the source again, but I remember reading that the average American doesn’t have enough money for an unexpected $500 expense, and are less than one paycheck away from defaulting on their mortgage / skipping their rent payment. That means the average American is no less protected from financial ruin by an Obamacare plan as they were from previous plans.

I could go on, but the absolute worst of it is that in exchange for very little reform of insurance company tactics, Obama gave away the one carrot we had to negotiate with insurance companies: the individual mandate. Now, the mandate is actually a good thing from a policy perspective, but still, you don’t give it up without driving a hard bargain in return. Giving it away for basically nothing in return means we no longer have any carrots left to force insurance companies to actually reform, which is why rather than take the “half a loaf” (as liberals like me were exhorted to do), I rather wished the whole thing failed and we try again.

FWIW, the people who are paying the penalty and going without insurance are making an absolutely rational economic choice: the NBER came out with a report last year that found that for people who receive little or no subsidies, purchasing Obamacare plans has a net *negative* effect on their financial status, regardless of assumptions used. Imagine that: health policies so awful that you’re better off paying almost a thousand dollars to avoid them! Sounds like the definition of junk insurance to me!

So I hope you understand why I actually wouldn’t mind if Republicans manage to overturn Obamacare, regardless of whether they have a replacement in mind or not. I used to think Democrats would do the right thing and pass medicare for all (the only plan that’s been proven to work in every other country in the world) if they had enough power but after watching Obama use a 60-vote supermajority in the senate and 60% strength in the House to pursue subsidies for private insurance, it seems regardless of who’s in control, the only way to wrest our politicians from their insurance company patrons is to burn the current system to the ground.

If you or a loved one develops a chronic or terminal illness, you will care. I agree changes are needed to the ACA, but throwing it out with no replacement – especially since that means Republicans are in control – will be a human disaster.

America is in a bad place right now – unable to agree on much of anything and lacking any interest in doing so into the future. Paul Ryan has a plan for health care in “A Better Way”. Look it up – especially if you are approaching retirement. Then imagine finding out you have Parkinson’s Disease, or cancer, or your child is born with a serious congenital medical issue….Average households simply can’t sustain the costs involved in caring for chronic, serious illnesses. The real solution is a consensus driven plan. Democrats tried and Republicans to a one, voted against the proposed plan while offering nothing along the way – EVEN THOUGH they were invited to do so time and again.

Be careful what you ask for, WX Wall. I know there are costly problems but the biggest problem are determining what our nation’s priorities are…health care is way down the list.

1mime-

I do care. But we already have a human disaster. And Obamacare is only prolonging it. People with chronic conditions do not do better under Obamacare, unless they are rich enough to afford the $6500 deductible. Otherwise, they are just as likely to face financial ruin as if they didn’t have insurance at all (or couldn’t get it pre-Obamacare). How many people with severe chronic conditions are healthy enough to earn a high enough salary that an annual $6500 expense is no big deal? And how many are healthy enough to continue to work in that high-pay job year after year?

The more common outcome is that once someone comes down with a severe illness, they can no longer work (or work as much). Soon (usually within the first illness event), they drain their savings, max out their credit cards and pawn their wedding ring to pay that deductible. After which, they can no longer afford the premium either, even at a subsidized rate. At which point, they’re back to square one.

Before or after obamacare, this is the trajectory you follow in America if you have a major illness and don’t have medicare: 1) pay for insurance until you get sick; 2) lose your insurance plan; 3) sell all your assets and go bankrupt; 4) go on medicaid. Obamacare switches the order of #2 and #3 (assuming you pay your premiums before the deductible exhausts your savings) but otherwise does not change the final conclusion (bankrupt, on medicaid).

The only ones who escape this trajectory under Obamacare are people rich enough to afford $6500 in medical costs per year *after* their premiums, and are somehow still healthy enough to continue to earn enough money to pay that outlay every year. And even those, must continue to run that race with their ever-increasing health burden until they either make it to 65 and get medicare; lose their job, go bankrupt, and go on medicaid; or die early. Obamacare does not change these end-results.

What is so frustrating about this, WX Wall, is that members of Congress who have refused to work across the aisle for health coverage, have a much better ACA policy. Personal bankruptcy due to medical reasons leads all categories and to me, this is unconscionable. I simply do not believe we have to throw it all out to develop a new, better plan. Sadly, I don’t think the Republican Party cares about fixing this problem, and they hold the purse strings in Congress. This is not a problem that can be easily or quickly resolved and it has to include both parties in order to come up with something that will be affordable, adequate, and sensible. Do you see this Republican majority leading the way to accomplish this?

Trackbacks

[…] featured post is my attempt to forget the campaign for a moment and worry about the nation: “What’s up with ObamaCare (other than premiums)?“. Next week’s Sift will come out the day before Election Day, so I’ll have my […]